MN Housing Programs

First-time home buyer (or have not bought a home in the last 3 years)? Visit MN Housing to learn if the Start Up Program is right for you! They also assist investors in multi-family units!

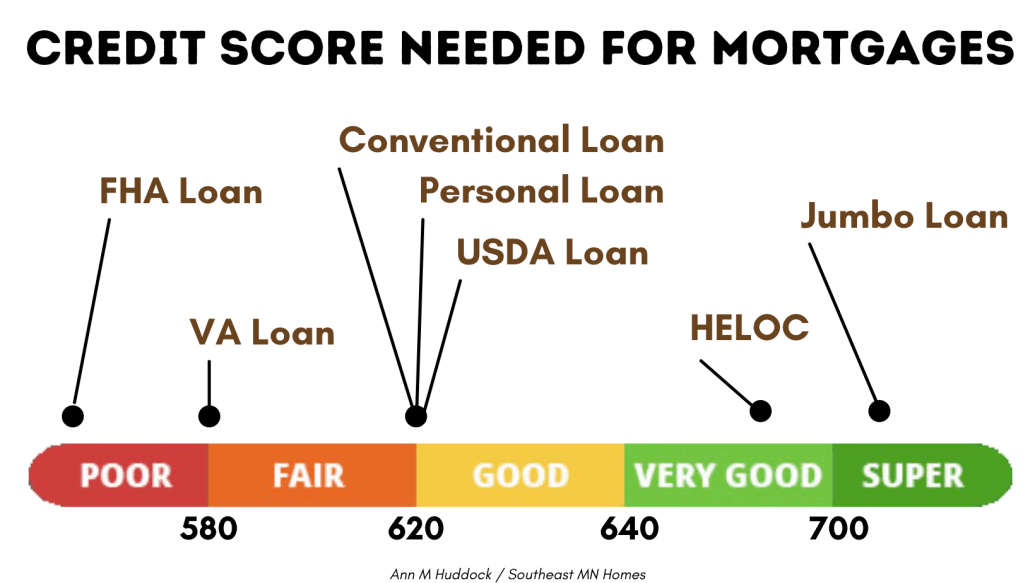

You have MANY options when it comes to financing. If you're like most home buyers, you likely know you need to take out a mortgage, but choosing between the different options can be as overwhelming as finding your dream home. Traditional mortgage options including Conventional, FHA, FHA's 203(k), USDA, and VA are the most common ways for people to afford a home. There are other options if your credit is less than perfect and I can help get you there.

There are so many unique ways to finance real estate it can be hard to fully understand what is available. Creative financing for real estate refers to uncommon or unique ways an individual can purchase land or properties that are for sale. I have years of experience assisting buyers with down payment assistance, contract for deed purchases, rent-to-own homes, and other creative financing techniques for all kinds of home buyers!

The bottom line: There are many things to consider when you want to finance a new home so you should partner with a REALTOR®️ and loan officer that you can trust.

Unless you are paying all cash for your new home, you will have to consider the type of financing you will need. Mortgage loans come in different shapes and sizes. A lender will work with you to get a loan that meets your needs.

Lenders will need to see documentation of your income, employment, two years of IRS filings if you are self-employed, bank accounts, 401(K) funds, and other assets. It’s smart to compile this before you even begin shopping for financing options. It’s also useful to have at least a rough idea of your current household expenses; they will affect the amount of mortgage you can obtain and the maximum price of the house you can finance. And don't forget! Request quotes from multiple lenders and comparison shop for loans.

Conventional loans are often the best option for borrowers with strong credit who can contribute a down payment of at least 3% or more. Credit score of 620 or higher is typically needed.

Conventional loans are often the best option for borrowers with strong credit who can contribute a down payment of at least 3% or more. Credit score of 620 or higher is typically needed.

The three main government-backed home loans are the Federal Housing Administration (FHA) Loan, the U.S. Department of Agriculture (USDA) Loan, and the Department of Veterans Affairs (VA) Loan. Lower down payment and credit score requirements.

If your credit is less than perfect or you prefer to leave big banks out of your purchase, there are other options! Contact me to discuss Rent to Own Leases, Right to Purchase Contracts, and Contracts for Deed.

Find your dream home, move in now, and rent with built-in savings for your down payment. In 3 years or less, you’re ready to buy. With Divvy, save up for your future down payment while renting, and take over when you’re ready–or just walk away. It's that easy! The application process is free, and fast, and won’t impact your credit score.

Not ready to buy or maybe you are just looking to rent a home that is currently on the market? Lease with Right to Purchase for up to 5 years. Click HERE to apply or search for qualifying homes or get more information below.

Over the past several years, contracts for deed have emerged as increasingly popular home-purchase arrangements for prospective buyers in Minnesota, particularly for those who lack the ability to obtain traditional financing. In a contract-for-deed transaction, the seller rather than a third-party lender finances the purchase of a property. Learn More.

Ready to Win?

It’s hard to keep losing out on the homes you want. Get a competitive edge and make your offer an all-cash offer. Sellers prefer accepting a cash offer over a traditional mortgage as it provides several advantages such as speed, cost savings, reduced time, and lower stress. A cash offer is simply a sale in which the buyer offers the seller the entire cost of the house without using financing, such as a mortgage loan. When a buyer already has enough funds to purchase your home outright, you can both avoid several (long, costly) steps.

If you don't have cash on hand to buy a home outright, no worries, you are like most home buyers! I work with many different companies to get you approved for a traditional mortgage so that they make a cash offer on your behalf to the seller and you are more likely to win your home by avoiding financing and appraisal contingencies.

First-time home buyer (or have not bought a home in the last 3 years)? Visit MN Housing to learn if the Start Up Program is right for you! They also assist investors in multi-family units!

The Wisconsin Housing and Economic Development Authority, or WHEDA, offers programs to make it easier for first-time home buyers. Check out a free homebuyer webinar and learn more!

Owning a home can be a big purchase and responsibility. Through the CDA’s homeownership programs and services, Dakota County residents have resources and information available to purchase a home, fix up their existing home, prevent their home from going into foreclosure, and make their home as energy efficient as possible. Their mission is "To improve the lives of Dakota County residents and enhance the economic vitality of communities through housing and community development."

The Goodhue County Down Payment and Closing Cost Assistance Program’s mission is to support working individuals and families in achieving homeownership. This will be achieved through providing individuals and families with access to a down payment & closing cost assistance program. The assistance will be in the form of a 0%, deferred loan. Eligible applicants will be able to qualify for up to $10,000 to be used toward the purchase of a home. Applicants will be served on a first come, first served basis.

Gravy helps renters save money, earn rewards toward their future house, and buy a home sooner. Different than most financial products, we obsess with one thing: helping you become a homeowner. It may not be as far away as you think. Gravy homebuyers save an average of 2% of the purchase price - that's $6,000 on a $300k house. Save for a down payment, build your mortgage credit score, learn about the process, and ultimately find and finance your new house––all in one place.

If you are a first-time homebuyer, you may need some assistance with coming up with cash for a down payment. There are several programs available and it only takes a few minutes to find out if you are eligible. Read Myths vs Facts on Down Payment Assistance or watch the video to learn more about how you can discover down payment assistance programs that can help you buy a home sooner than you might think!

Check to see if you are eligible HERE.

Estimate a mortgage payment based on the price of a home and a down payment you can afford.

How much of a down payment should you make? Compare different options to explore what down payment level is better for your needs.

Determine the affordability of a new home loan based on a monthly payment within your budget.

Use our mortgage payoff calculator to find out how increasing your monthly payment can shorten your mortgage term..

Should you wait a few more years to save up for a big down payment, or is it smarter to buy right now?

Wondering if continuing to rent or buying a house is better for your wallet? Compare the cost of renting vs. owning a home.

Your credit scores help determine which loan programs you’re eligible for, as well as the interest rate you qualify for. Higher credit scores generally mean more financing options and potentially better interest rates for you. It's essential if you are planning to apply for a mortgage that you know your credit score.

Federal Law allows for you to get a free copy of your credit report every 12 months from each credit reporting company. There is only one authorized website from which you can request this. I also personally recommend signing up for Credit Karma. While the score given is a VantageScore and not a FICO score (what 90% of lenders use), it still is a valuable (and free!) tool for monitoring your credit report and becoming educated on how to improve your score.

Hello, my name is Aaron Neubauer and I have been in the mortgage industry for 16 years. My local market is Minnesota Twin Cities Metro and surrounding areas. I am also experienced in many mortgage specialties and am prepared to answer any and all questions that clients have for me. My favorite part of working with homebuyers is being able to assist in educating them so that they can make the best decisions for their goals. I strive to be a source of knowledge for all of my clients and I also strive to always be available for their questions.

Outside of the office, I love staying active. I spend a lot of time outdoors and love to play sports. I also am fond of cooking and volunteering to better others situations. My volunteering includes coaching basketball and I also try to do something once a year for MS society as well as Make-a-Wish.

I look forward to the opportunity of working with you. Contact me today to get started on your homebuying journey! NMLS #333209

📧 aaron.neubauer@successlending.com

☎️ 612-644-4265

Whether you’re buying, selling, refinancing, or building your dream home, you have a lot riding on your loan specialist. Since market conditions and mortgage programs change frequently, you need to make sure you’re dealing with a top professional who is able to give you quick and accurate financial advice. I have the expertise and knowledge you need to explore the many financing options available.

Ensuring that you make the right choice for you and your family is my ultimate goal. And I am committed to providing my customers with mortgage services that exceed their expectations. I hope you’ll browse my website, check out the different loan programs I have available, use my decision-making tools and calculators, and apply for a loan in just four easy steps with the short form Application.

After you’ve applied, I’ll call you to discuss the details of your loan, or you may choose to set up an appointment with me using my online form. As always, you may contact me anytime by phone, fax or email for personalized service and expert advice. NMLS #1483659

📧 jennylee.fahey@edgehomefinance.com

☎️ 651-270-0799

© Copyright 2020-2025 Southeast MN Homes LLC

All Rights Reserved